You are a valued member of our community and together we make the accounting profession sparkle. We have a wide variety of opportunities to connect, innovate, advocate, and learn together. KSCPA is your personalized access point to experts, reliable facts, leadership, and social connections.

We've accomplished a lot the last few years, balancing these uncertain times with reasons to celebrate our important work of keeping our profession bright in Kansas.

Our Important Work

Conferences, timely webcasts, and unique membership events designed to move your career and the profession forward, together.

KSCPA featured events are designed to keep you informed and engaged when it comes to the most important topics in the profession.

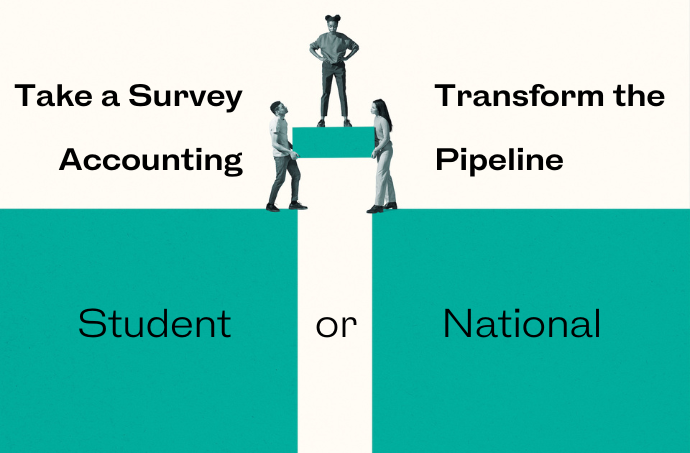

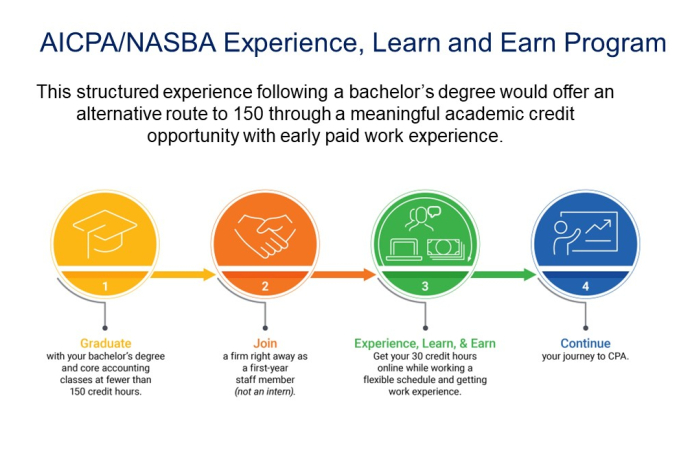

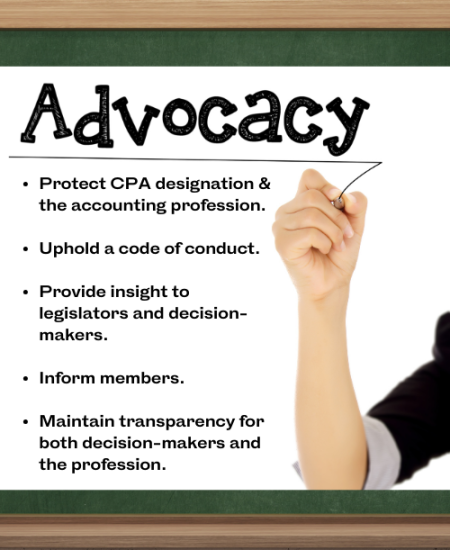

KSCPA is the only organization advocating and protecting the future of Kansas CPAs. Our advocacy efforts start with attracting and building the talent pipeline of future CPA leaders, while keeping a pulse on legislative activity and providing expertise to legislators.

Learn More

Leadership is a function of seven BIG IDEAS: Serve Others, Be Generous, Have Integrity, Create Community, Pursue Excellence, Exhibit Graciousness, and Understand Hope. The IDEA that resonates with me the most is Understand Hope. Hope has an author who provides us with the power to believe that anything is possible. Hope is knowing that the circumstances we face are temporary, opportunities we encounter are endless, and as long as we believe, anything can happen!

I believe strongly in lead by example. If you want your team to act with integrity, you must exhibit it too. If you want your team to innovate, you must open your mind to different ideas and be willing to listen to them.

Leadership has never been more important to the accounting profession than it is today. With an ever-evolving landscape, and hurdles to overcome that the profession hasn’t seen before, we all must take an active role in highlighting the opportunities our profession can provide. Leadership encompasses expertise in subject matter areas, making decisions…for our teams, clients, ourselves and future generations, having interpersonal skills to further develop relationships, being able to resolve conflict and, maybe most importantly, having courage to not be satisfied with the status quo! Effective leadership will continue to mold the accounting profession in to an exciting and rewarding career path for all!

Meaningful innovation is a process that is enhanced and refined over time when there is a future state in mind. It is critical for today's leaders to be forward thinking, with a willingness to accept and learn from mistakes in the process, in order to achieve optimal success.

© Copyright 2024 KSCPA | All Rights Reserved